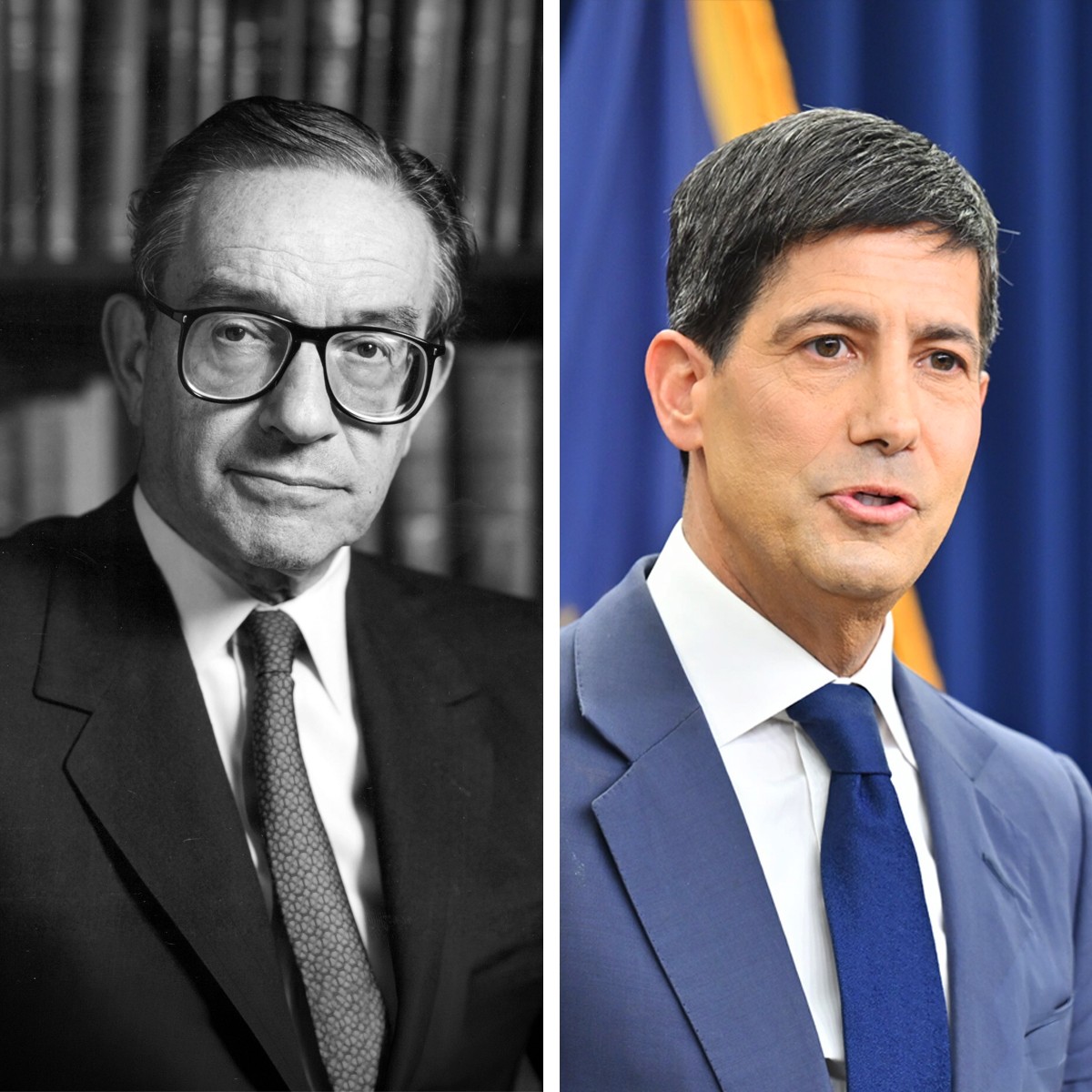

Alan Greenspan passed away this week at 100 years old. He served four presidents, led the Federal Reserve through some of the most consequential decades in modern economic history, and became, in his own distinctive way, one of the most influential figures American finance has ever produced. His passing prompted me to spend some time thinking, not just about his legacy, but about what it might tell us about the moment we are in right now.

Because timing, as it so often does in markets, has a way of meaning something.

Kevin Warsh has just taken the chair that Greenspan once held. The two men are separated by decades, but when I look at the circumstances surrounding each of their tenures, I find the parallels striking enough to be genuinely instructive for investors trying to make sense of where we go from here.

Before examining those parallels, it is worth restating what the Fed is actually charged with doing. Congress has given the Federal Reserve a dual mandate: promote maximum employment and maintain stable prices. Of course, price stability is closely associated with low and stable interest rates. These goals are frequently in tension, and how a Fed chairman navigates that tension defines his legacy.

The environment Warsh inherits makes that navigation unusually demanding. United States debt is approaching $39 trillion. The Fed’s own balance sheet, still carrying the weight of post-pandemic asset purchases, has left the institution in a structurally unusual financial position. A cohort of major central banks appears increasingly inclined toward gold over Treasuries. And then there is the wildcard of a technological transformation that could fundamentally reshape employment and corporate efficiency in ways the historical playbook does not fully account for. Any one of these would define a chairmanship. Warsh faces all of them simultaneously.

With that backdrop in mind, here are three parallels to Greenspan that I think are worth watching closely.

The Art of Saying Less

Greenspan was famously opaque. He understood, perhaps better than any Fed chair before or since, that a central banker’s words carry weight precisely because they are scarce. He did not telegraph moves. He did not publish dot plots. He did not hold press conferences designed to manage expectations quarter by quarter. While forward guidance and publication of Fed minutes were both initiated on his watch, he preferred surprise — a well-timed cut or raise that the market hadn’t fully priced in — because surprise, deployed judiciously, actually works. It gets traction. It moves behavior.

He once said, only half-jokingly, that if his remarks seemed clear, he had probably been misunderstood.

We have spent the better part of the last fifteen years moving in the opposite direction. The Fed has become a communications operation as much as a monetary policy institution. Dot plots, post-meeting press conferences, explicit signaling of intention: all of it designed to reduce uncertainty. The problem is that when the forecasts miss, and they often do, credibility takes a hit. Markets learn to discount the guidance. The tool loses its edge.

Warsh has signaled clearly that he wants to pull back from this approach. He demonstrated an independent streak in his very first press conference, something the market did not fully anticipate. He is not interested in managing every expectation. He would rather be a Fed chair whose actions mean something because they are not entirely predictable. That is a meaningful philosophical shift, and I think investors would do well to internalize it.

Letting the Market Do Its Work

There is a second parallel that receives less attention but may matter just as much over time. Greenspan did not use the Federal Reserve’s balance sheet as a backstop for the Treasury market. Large-scale asset purchases, what we now call quantitative easing, were not a tool of his era. That instrument was introduced by his successor in the aftermath of the 2008 financial crisis and has since become so embedded in market expectations that many investors treat Fed balance sheet support as a permanent feature of the landscape rather than an emergency measure.

Warsh has spent years pushing back against that assumption. His writings and public statements reflect a genuine philosophical conviction that Treasury pricing should be more a function of market forces and less a function of central bank intervention. He has been a consistent critic of balance sheet expansion, arguing that it distorts price discovery and creates dependencies that make the eventual normalization more painful. His preference, stated plainly, is to let the market reassert itself.

That would represent a meaningful departure from the post-2008 model and a return, in spirit, to how Greenspan operated. For bond investors in particular, it is a posture worth taking seriously.

The Technological Tailwind

There is a third parallel that I find equally compelling, and it may ultimately matter more than either of the first two.

When Greenspan took the helm in 1987, the personal computing revolution was just beginning to show its economic hand. Through the late 1980s and into the 1990s, the proliferation of desktop computing, enterprise software, and eventually the internet began doing something that traditional economic models struggled to fully account for: it made the economy more efficient at a structural level. Productivity gains were real, durable, and broad-based. That gave Greenspan significant latitude. Growth could run warmer than historical norms suggested without triggering the inflation that orthodox models would have predicted. The technology was doing some of the work that monetary policy might otherwise have needed to do.

I think Warsh may find himself in a structurally similar position.

Artificial intelligence is not a passing cycle. It is a fundamental reorganization of how work gets done, how capital gets allocated, and how value gets created. The same is true of quantum computing, which promises to compress timelines for discovery and problem-solving in ways we are only beginning to model. The buildout of data center infrastructure is already one of the most significant investment cycles of the last several decades. And beyond the purely digital, we are watching a serious push toward space-based industry, with missions to Mars no longer existing only in the realm of aspiration.

These are not speculative themes. They are already showing up in earnings, in capital expenditure, in small-cap performance. The Russell 2000 has roughly doubled the S&P 500’s return so far this year, in part because the ecosystem around AI infrastructure is lifting a broad range of businesses beyond the handful of household names that defined the early innings of this cycle. That kind of breadth is a signal worth taking seriously.

When technology is genuinely driving structural productivity gains, an economy can sustain stronger growth with less inflationary pressure than the historical playbook would suggest. Greenspan understood that dynamic intuitively, even when his contemporaries were skeptical. It gave him room to operate. Warsh, if he reads the current technological moment correctly, may find he has more room than the consensus currently expects.

The Constraint Greenspan Never Faced

There is, however, an honest caveat that intellectual fairness requires.

Greenspan’s deflationary tailwind operated in a fiscal environment that bears almost no resemblance to today’s. Federal debt during his tenure was a fraction of current levels. The Fed’s balance sheet was modest. Deficits, while present, were not structural in the way they are now. The latitude that technology provided him was relatively unconstrained by the fiscal backdrop.

Warsh does not have that luxury. The AI-driven productivity gains may be real and durable, but they are working against a fiscal drag of historic proportions. Whether that tailwind is large enough to offset the headwind is the central question of his chairmanship. It is not a question anyone can answer with confidence today. But it is the right question to be asking, and investors who frame it that way will be better positioned than those who assume the Greenspan analogy holds cleanly from beginning to end.

It does not. But the parts that do hold are worth understanding.

Rick Pitcairn is Chairman and Chief Global Strategist at Pitcairn. The views expressed are those of the author as of the date of publication and are subject to change. This commentary is for informational purposes only and should not be construed as investment advice.